The top five international semiconductor stocks recorded an average return on investment (RoI) of 100.59 percent between 28th June 2020 and 28th June 2021. Experts are of the view that Covid-19 might have accentuated the peak of the semiconductor industry. But there seem to be many more factors.

Semiconductors are to electronics what oxygen is to living beings. While helping control the flow of electricity in a circuit, these are known as the brain behind modern electronics.

Their importance to the world today could be mined from the fact that several automakers, smartphone OEMs, consumer electronic OEMs, and many others into electronics manufacturing have had to halt operations for some part of 2020 and 2021 due to shortage of semiconductors.

Further, despite lockdowns announced by almost all the countries following the outbreak of coronavirus, many semiconductor fabrication units were allowed to operate. International Data Corporation (IDC) recently noted that the size of the global semiconductor market will reach $522 billion in 2021. This represents a growth of around 12.5 percent year-on-year.

The proof of the pudding can also be gauged from the fact that the top five semiconductor stocks have recorded an average RoI of 100.59 percent between 28th of June 2020 and 28th of June 2021. The data collected and analysed by Finbold also shows that the top ten selected semiconductor stocks recorded an average RoI of 78.79 percent during that period.

“There are two metrics that the investors or top management of a fab need to be worried about. One is what the load of the fab is and second is what is the yield on the fab. ‘Load’ is the function of demand or a company’s capability to sell the 30K to 40K wafer starts per month. ‘Yield’ is how good are the number of ‘usable’ chips from each 300mm wafer. The fabs which have made the chips of these high performing companies are very mature ones.

They have already solved the yield problem on the well established and mature nodes, which is where the extraordinary growth is coming from. These fabs have also made significant investment into tooling for the newer nodes, which is where future demand will come. Note that in a good year a fab is a money printing machine,” says PVG Menon, former President of the India Electronics & Semiconductor Association (IESA), and former CEO, Electronic Sector Skills Council of India (ESSCI).

He adds, “Fabs announcing 100s of billions of dollars in R&D is proof in itself that fabs are money generating machines. Someone like a TSMC will not commit big amounts to R&D and capacity expansion unless it has demand (‘Load’) commitment from the likes of large-volume customers like Apple . Investing in a new node means investing at least $4 billion per node.”

Shortage and high demand

Starting 2020, semiconductors have been in high demand and, despite many fabs being allowed to function amidst coronavirus lockdowns, their supply in the market continues to be scarce. This is primarily due to the constraints the semiconductor supply chain went through, and continues to go through, due to the lockdowns. After all, fabricating semiconductors is one thing and getting them delivered to organisations is another!

In plain economics, obviously, a market shortage occurs when there is excess demand. In such situations, customers are usually unable to buy as much as they require, neither are the manufacturers able to meet all the demands. Even though most of the semiconductor companies were not able to keep up with the demand of the semiconductors, their share prices continued to, and continue to, grow as of today.

“There is huge demand for semiconductors, and it is clear from every part of the supply chain that there are shortages. There is a very big gap between the demand and supply. It is quite possible that customers are paying higher prices to source semiconductors than what they have been usually paying in the normal times,” says Hemant Mallapur, co-Founder, Saankhya Labs.

He adds, “This works in favour of both fabless as well as fab semiconductor companies. Primarily, if you trace it back to the origin, you will find that during the first wave of Covid-19 there was a big slump in demand. Immediately the people noticed that such things can hammer their business. Also because of the backlog many companies ordered semiconductors in amounts more than what they would normally buy.”

The shares of Nvidia, a fabless semiconductor company, yielded 107.87 percent RoI during the one year period under review. By fabless, as most of you know, we mean a semiconductor company that owns the IP but does not own a semiconductor fab. Such companies outsource semiconductor manufacturing to vendors like Taiwan Semiconductor Manufacturing Corporation (TSMC).

Nvidia had a market cap of $474.25 billion on 28th June 2021. Its stock price rose from $366.2 per share (June 2020) to $761.24 per share (June 2021).

Similarly, shares of Qualcomm, another fabless company, delivered approximately 56.38 percent RoI during the time frame. As a matter of fact, fabless semiconductor firms represented 32.8 percent of the total market in 2020, a record for the segment, according to data from IC Insights.

Qualcomm had a market cap of $155.27 billion on 28th June 2021. Its stock prices rose from $88.02 per share (June 2020) to $137.65 per share (June 2021).

The new record for market share for fabless companies was led by Qualcomm’s $5 billion sales increase in 2020. IC Insights has also forecast that fabless companies and IC foundries will continue to be a strong force in the total IC industry landscape with a percentage share of the total IC market expected to reach the mid-30s in the next five years.

This shortage of semiconductors can primarily be linked to various factors including restraints in supply of raw materials used to manufacture these, restraint in supply chain that supplies semiconductors to customers, and high demand of these due to increased production of electronics.

“The demand for semiconductors is being driven by everything that has a connection with the end consumers. The increased demand of wearables, especially devices like pulse oxymeters, fitness bands, and smartwatches. The explosion in demand for computing devices like laptops, tablets, and smartphones due to massive increase in both work and study from home, is another factor. Then there is demand for relatively newer gadgets (in India) like dishwashers coming in. We are spending more and more on smart gadgets,” explains PVG Menon.

The 5G factor

The advancement of 5G is leading to a more connected world than ever. And enabling electronics with better connectivity features requires better and the latest technology based semiconductors. As the 5G technology continues to spread over different parts of the world, electronics manufacturers will want to phase out existing devices based on 4G tech, and the process will require sourcing more and better semiconductors.

A report by Accenture, cementing this notion, has forecast that starting 2023, smartphones with 5G capability will sell more than 4G-compatible smartphones. As against 614 million 4G smartphones forecast to sell in 2023, a total of 995 million 5G handsets have been forecast to sell in that year. These numbers will keep on increasing to 1,143 million 5G handsets in 2024 compared to 470 million 4G handsets same year.

“The 5G has not gone up in volumes in terms of deployment by operators. But 5G demand is going to increase during the next couple of years, and products for it would ramp up in the coming years,” says Hemant.

The chip volume and RF frontend modules for 5G and 5G mmWave are expected to double in premium smartphones, and 5G semiconductor revenue—including baseband processors, RF, and power management—will increase from near zero in 2018 to $31.5 billion in 2023, the vast majority of which will be driven by smartphones.

A report by PMI has forecast that the global 5G semiconductor solutions market would be worth US$10.8 billion by 2029. It was valued at around US$1.5 billion in 2020. The growth and development in the ICT sector to improve wireless data networks, communication technologies, and solutions through fifth-generation network usage are expected to fuel the growth of the global 5G semiconductor solutions market.

This simply means that 5G is helping to increase the adoption of the latest tech based semiconductors in the world, and it is a known fact that products based on latest technologies usually cost more than the outdated or soon to be outdated technologies. Replacement of devices compatible with 4G by those compatible with 5G is also leading to an increase in the demand of semiconductors. However, as a lot of fabs are still struggling to update to the latest tech, there continues to be a shortage of the same in the market.

The shares of TSMC, a manufacturing vendor for a lot of fabless semiconductor companies, have delivered 106.87 percent RoI during the last one year. TSMC operates more than one fab based on the latest technologies and it is known as one of the fabs to always be on the top of the technology game. The company is targeting to start volume production using its latest 3nm tech in the second half of 2022.

TSMC had a market cap of $604.33 billion on 28th June 2021. Its stock prices rose from $56.33 per share (June 2020) to $116.53 per share (June 2021).

Automotive, EVs, and battery industry

A lot of experts and consulting organisations are of the view that the period of 2021 to 2030 will be the decade of electric vehicles (EVs). India and many other countries have already announced aggressive policies to increase the adoption of EVs. The global sales of EVs in 2020, as per a report by Canalys, increased by 39 percent in a year to 3.1 million units. This is when the total passenger car market declined 14 percent.

Canalys has also forecast that these figures will climb to 30 million EVs sold in 2028. EVs are expected to represent nearly half of all passenger cars sold globally by 2030. Now there is no rocket science in knowing that the more sophisticated an electric car model is, the more semiconductors are required to power it.

“EVs being very hot right now, there is already very high demand from the sector. Automotive uses a large number of sensors and electronics now. I think the sector has also contributed to the increased demand of semiconductors,” explains Hemant.

Global demand for automotive semiconductor market, in terms of revenue, was worth $45.98 billion in 2020 and is expected to reach $81.40 billion in 2027 (Brandessence Market Research). As a matter of fact, even ICE powered vehicles enabled with security features like camera and connectivity require a good number of semiconductors. Moreover, as the autonomous driving feature starts becoming more common, the quantity of semiconductors demanded by automotive OEMs will see an even sharper incline.

Since 2020, automotive OEMs have been ramping up the production of EVs and hence demanding more and more semiconductors from companies. The likes of Audi have already announced to be EV-only brand by 2026.

Batteries and charging points are two other industries that are directly related to the EV ecosystem, and both of these require semiconductors in good numbers. Batteries require semiconductors because developments in the semiconductor arena can help provide longer battery life and range, and charging points because they are all electric.

“With congestion in the public transport sector, a lot of people are investing in buying private vehicles. Remember the amount of electronics in these vehicles. Forget about high-end cars and talk to Maruti and you will be surprised to know the number of electronics items that go into an entry segment car like Alto 800,” says Menon.

“Then look at two-wheelers and you will find semiconductors worth at least $7-8 going into an entry level two-wheeler. The mandating of Bharat Stage-6 emission standard for all vehicles has added to the semiconductor BoM in two-wheelers. Note that in higher end two-wheeler models, the semiconductor BoM is much higher as the vehicle has a sophisticated ECU, multiple sensors, etc. All of this has pushed up semiconductor consumption in the petrol two-wheeler segment. EVs have even more electronics and semiconductor components,” says Menon.

India, one the fastest developing countries in the world, has announced a production linked incentive scheme worth 181 billion rupees dedicated towards promoting ACC battery manufacturing in the country.

“From a market size perspective, India produced around 25 million two-wheelers in 2019. As we see more functionality getting added in terms of sensors, controllers, communication protocols, entertainment options, etc, the semiconductor and electronic BoM is going to sharply increase in the days ahead,” Menon explains.

The shares of NXP Semiconductors, one of the leading suppliers of automotive semiconductors and solutions, delivered an RoI of 88.78 percent during the last one year. The company’s market cap as of 28th June 2021 was around 56.3 billion dollars. The stock price for NXP rose from $108.15 per share (June 2020) to $204.17 per share (June 2021).

The US, China, and India

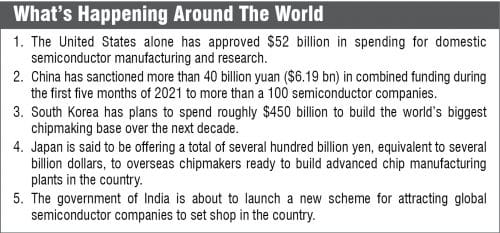

The increasing importance of semiconductors can easily be gauged from how the world’s superpowers as well as India are making efforts to enable a superior local semiconductor ecosystem in their respective geographies. For starters, the USA alone has approved $52 billion in spending for domestic semiconductor manufacturing and research as an important step towards strengthening the country’s leadership in the industry.

“We are in a competition to win the 21st century, and the starting gun has gone off,” the US President Joe Biden has said in a statement recently.

He added, “As other countries continue to invest in their own research and development, we cannot risk falling behind. America must maintain its position as the most innovative and productive nation on Earth.”

Similarly, India, one of the fastest developing countries in the world, is also working on envisaging a plan to facilitate the semiconductor ecosystem in the country. It is expected that the government of India will approach setting up of a fabless cum ATMP/OSAT ecosystem soon by offering handsome incentives to global heavyweights.

China, on the other hand, has already given more than 40 billion yuan ($6.19bn) in combined funding during the first five months of 2021 to more than 100 semiconductor companies. According to a report by Research and Markets, the investments in new fabs or capacity expansion will exceed US$160 billion in China over the coming 5-7 years. This is expected to drive an increase in China’s equipment spending to more than $40 billion in 2025, with sixty percent of the investments going to memory fabs.

All semiconductor companies, whether fabless or fab, have been spending billions of dollars in researching and developing the latest avatar of semiconductors and processes that enable faster and efficient manufacturing. In a recent interaction with Sunil Banwari, Advantest Corporation, we learnt that the top semiconductor producers are exploring industry 4.0 manufacturing capabilities in order to combine them with semiconductor design and fabrication.

“The shortage is likely to continue at least till the middle of the next year. That definitely fuels this trend that you have unearthed. With AI and 5G picking up, I think the market is going to be good for them. What Covid has done is accentuated the peak of the semiconductor industry,” says Hemant.

While the semiconductor industry is cyclical in nature, at the moment it seems far away from witnessing a down curve, primarily because the demand for modern electronics has just started going up. For investors it might be a good idea to invest in shares of such companies, but for governments it would be a good idea to go all guns blazing towards creating a superior semiconductor ecosystem.

Mukul Yudhveer Singh is a business journalist at EFY